Budget day creates an expectancy of relief and concerns about the additional burden of taxes. The indirect tax budget announcements for 2023, however, neither provided much relief not added a significant burden of taxes. Nevertheless, it is important to understand the amendments proposed through Finance Bill, 2023 to GST law.

1. Amendments in the composition scheme

Section 10 of the CGST deals with the composition scheme, applicable for small suppliers. The said scheme is not applicable to certain categories of suppliers, one of which being, any supplier effecting supplies of goods or services, through E-commerce operators. Now this restriction has been removed and suppliers of goods though E-commerce operators have been allowed to opt for composition scheme and the prohibition will apply only for suppliers of services.

2. Amendment in Section 16

Prior to amendment, as per the second provision under sub-section (2) of section 16, any taxable person who has availed Input Tax Credit (ITC) shall pay the value Of supply and tax thereon to the supplier, within 180 days from the date of invoice, failing which the ITC availed “shall be added to his output tax liability along with interest”. The same has been amended to “Payable along with Interest under section 50 CGST Act”. The change is only semantic and the liability to reverse the credit continues as such.

3. Amendment in Section 17(3) CGST Act

Value Of activities as may be prescribed in respect of warehoused goods before their clearance for home consumption will be considered as exempt supplies for the purpose of common ITC reversal.

4. Insertion in Section 17(5) (fg) CGST Act

Section 17(5) (fa) is being inserted to block ITC on goods or services or both received by a taxable person, which are used or intended to be used for activities relating to his obligations under corporate social responsibility referred to in section 135 of the Companies Act, 2013. It has been specifically provided that ITC of taxes paid on goods and services which are used in discharge of Social Responsibility Corporate obligations under the Companies Act is not admissible. It may be noted that in view of this specific amendment, such ITC is admissible, till the amendment comes into effect.

5. Person not liable for registration

Section 23 of the Act lays down that, any person who is exclusively engaged in making non-taxable supplies or exempt supplies; and agriculturalists are not required to obtain registration.

• Section 22 of the Act which deals with registration lays down any person whose aggregate turnover exceeds the minimum threshold limit is liable to be registered.

• Section 24 of the Act makes registration compulsory in certain cases.

To this extent, there is an incongruity in the provisions and a person who is not liable to be registered under Section 23 may require registration if he fulfils any of the conditions under Section 22 or 24. In order to remove this anomaly, the provisions of Section 23 has been made as non obstante, the provisions of Section 23 shall prevail.

over Section 22 and 24.

6. No return to be filed after three years

Section 37 dealing with return of outward supplies (GSTR-I), Section 39 dealing with

monthly return (GSTR-3B), Section 44 dealing with annual return (GSTR-9 / 9C) and Section 52 of the Act dealing with filing of return by Electronic Commerce Reporter who is liable to collect tax at source, have been amended to the effect that no such return shall be required to be filed after the expiry of three years from the due date for filing such return.

The present dispensation requires that any return can be filed only if the said return for the preceding periods are filed. Non filing of returns also attracts late fee. By virtue of these amendments, if the above returns are not filed for a period of three years from the due date, there is no requirement to file such return and the taxpayer can proceed to file the subsequent returns. However, this will not erase the liability to pay any tax for the said period, which can be recovered under Section 73 or 74. This amendment will provide some relief from payment of huge late fee.

7.Provisional refund eligible for provisionally-accepted-ITC

Section 54(6) has proposed to be amended, refund of 90% of refund so claimed was earlier reduced by the ITC Provisionally accepted now the exclusion is removed. Hence 90% of refund in case of zero-rated supplies made.

8. Interest on delayed refund

If any tax ordered to be furnished to any applicant is not refunded within 60 Days from the date of receipt of application, interest at such rate not exceeding 6% as may be specified, in the notification issued by the govt. on recommendation of GST Council shall be payable in respect of such refund for the period of delay beyond sixty days from the date of receipt of such application till the date of refund to be computed in such manner and subject to conditions and restrictions as may be prescribed.

9.Amendment in penal provision for E- Commerce Operator

A new sub section (1B) in section 122 of CGST Act is being inserted to provide for imposition of penalty on E-commerce operators, who,

(i)allows supply of goods or services by an unregistered person through such Electronic Commerce Operator.

(ii)allows making inter-state supply, where it is not permitted (a supplier of goods through E-commerce operator can now opt for composition scheme. But under composition scheme, making inter-state supply is prohibited); and

(iii)fails to furnish correct details in the return.

Shall be liable to pay a penalty of ten thousand rupees or an amount equivalent to the amount of tax involved had such supply been made by registered person other than a person paying tax under section 10, whichever is higher.

10. Decriminalisation

The following offences would no more be punishable with imprisonment.

• Obstructing or preventing any officer in the discharge of his duties under this Act; tampering with or destroying any material evidence or documents.

• failure to supply any information which he is required to supply under this Act, or the rules made thereunder or suppling false information; and

• attempting to commit or abetting any of the above offences.

The following punishment are prescribed under sub-section (1) of Section 132.

(i) in cases where the amount of tax evaded or the amount of input tax credit wrongly availed or utilised or the amount of refund wrongly taken exceeds five hundred lakh rupees, with imprisonment for a term which may extend to five years and with fine.

(ii) in cases where the amount of tax evaded or the amount of input tax credit wrongly availed or utilised or the amount of refund wrongly taken exceeds two hundred lakh rupees but does not exceed five hundred lakh rupees, with imprisonment for a term which may extend to three years and with fine.

(iii) In the case of any other offence where the amount of tax evaded or the amount of input tax credit wrongly availed or utilised or the amount of refund wrongly taken exceeds one hundred lakh rupees but does not exceed two hundred lakh rupees, with imprisonment for a term which may extend to one year and with Fine.

Clause (iii) above has been amended and the words “any other offence” is substituted with “an offence specified in clause (b) which deals with issuing fake invoice. As a result of this amendment, for any offence other than issuing fake invoice, the minimum threshold for launching prosecution is Rs. 2 crores.

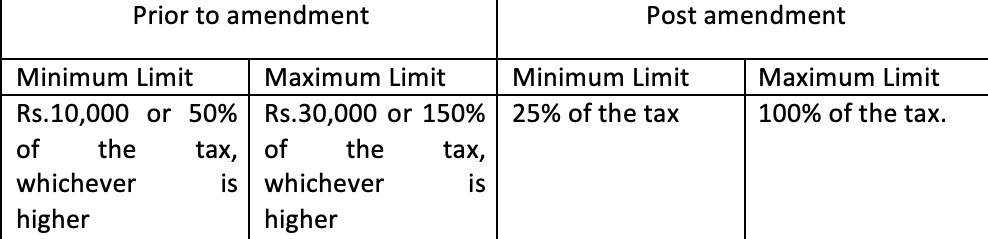

11. Changes in compounding provisions

As per Section 138 of the Act, any offence under the Act can be compounded by paying the prescribed compounding amounts. The said Section also contains certain restrictions for claiming the benefit of compounding. The minimum and maximum limits on the compounding amount have been amended as below.

The decriminalised offences are removed from compounding scheme. This is consequential amendment.

Clause (a) of sub-section (1) of Section 138 provides that a person who has once compounded any offence under clauses (a) to (f), (h), (i) and (l) of sub-section (1) of Section 132 shall not be allowed to compound such offence once again.

Clause (b) of sub-section (1) of Section 138 provided, second time compounding of any other offence is not allowed.

This restriction is now removed. Person committing the offence of issue of fake invoice cannot opt for compounding.

12. Retrospective effect to certain amendments in schedule III

Para 7 and 8 have been added in Schedule Ill, with effect from 01.022019. Hence these transactions would not at all be considered as a supply and no GST is payable. The said paras are reproduced below.

7. Supply of goods from a place in the non-taxable territory to another place in the non-taxable territory without such goods entering into India.

8. (a) Supply of warehoused goods to any person before clearance for home

consumption.

(b) Supply of goods by the consignee to any other person, by endorsement of

documents of title to the goods, after the goods have been dispatched from the port of origin located outside India but before clearance for home consumption.

Now, retrospective effect is being given to these amendments from 01.07.2017. But if anybody has paid GST on such transactions, before they are placed under Schedule Ill, no refund can now be claimed.

13. Omission of proviso Section 12(8) of IGST Act

Section 12 (8) of the IGST Act, reads as below:

12(8) The place of supply of services by way of transportation of goods, including by

mail or courier to, –

(a) a registered person, shall be the location of such person.

(b) a person other than a registered person, shall be the location at which such goods are handed over for their transportation. As per the above, the place of supply of the

services of transportation of export consignment of an Indian exporter, by an Indian transporter would be in India and attract GST.

The following proviso was added to the said sub-section, with effect from 01.02.2019. Provided that where the transportation of goods is to a place outside India, the place

of supply shall be the place of destination of such goods. By virtue of this proviso, the place of supply in case of transport of export consignments would be outside India, i.e., the destination. As per Section 7 (5) (a) of the IGST Act, when the supplier is in India and the place of supply is outside India, it shall be an inter-state supply and attract IGST.

But vide S.Nos. 20A and 20B of Notification 9/2017 Integrated Tax (Rate) Dt. 28.06.2017, as introduced vide Notification 2/2018 Integrated Tax (Rate), Dt. 25.01.2018, exemption from payment of GST for such transportation service was granted up to 30.09.2018, which was extended from time to time, up to 30.092022. The said exemption was not extended from 01.10.2022 and hence export freight became taxable from this date.

Now, the above proviso has been omitted and the place of supply for transportation services, where both the supplier and recipient are situated in India, would be determined as per subsection (8) of Section 12, without this proviso. If the recipient of the service is registered, the place of supply shall be the recipient’s location and if the recipient is not registered the place of supply shall the location at which the goods are handed over transportation.

14. Amendment in definition of ‘non- taxable online recipient’ and ‘OIDAR’

Presently, “non-taxable online recipient” is defined to mean any Government, local authority, governmental authority, an individual or any other person not registered online and receiving information and database access or retrieval services in relation to any purpose other than commerce, industry or any other business or profession, located in taxable territory.

It is now proposed to amend definition of ‘non-taxable online recipient’ to mean any unregistered person receiving OIDAR services located in taxable territory. Term ‘unregistered person’ in above definition includes a person who is registered solely for the purpose of deducting TDS under the GST Act.

Requirement of OIDAR services to be ‘essentially automated and requiring minimal human intervention’ has been removed from the definition Of OIDAR Service.

15. Consent based sharing of information furnished by taxable person

A new section 158A in the CGST Act is being inserted so as to provide for prescribing

manner and conditions for sharing of the information furnished by the registered person in his return or in his application of registration or in his statement of outward supplies, or the details uploaded by him for generation of electronic invoice or E-way bill or any other details, as may be prescribed, on the common portal with such other systems, as may be notified.

Interested in this topic or wanting to know more? Share your thoughts and we will be happy to assist.